The First Real RWA Bridge:Why Private Credit Broke the Barrier Between TradFi and DeFi

Most tokenized assets stop at the wrapper. They are issued, distributed, and then sit in static positions in wallets, producing yield on paper but doing nothing within the financial system they claim to be part of. That's not a bridge between TradFi and DeFi. That's a filing cabinet with a blockchain address.

Private credit did something different. And understanding why it moved first tells you almost everything about where the rest of the RWA market is actually going.

The Reason Was Always the Yield

Private credit fits on-chain earlier than most asset classes for a reason that sounds obvious once you say it: it already has something crypto markets know how to price. Yield, that predictable, distributable, near-term cash flow — the kind of thing DeFi was built to route, collateralize, and recycle.

Private credit is now the largest RWA category on-chain, with approximately $12.9B in active loans — ahead of tokenized T-bills at $6.2B, commodities at $1.4B, and tokenized equities at $484M.That ordering isn't accidental, since it reflects a fundamental compatibility between what private credit produces and what on-chain markets can consume.

Compare that to the other categories everyone assumed would tokenize first. Moreover, private equity is mostly about access and long-duration exposure. Venture capital is illiquid by design, with returns that arrive years later and can't be financed against. Real estate has valuation, liquidity, and jurisdictional complexities that tokenization doesn't solve but only repackages. None of them offer what private credit offers: a yield stream that can be distributed monthly, used as collateral, and plugged into lending markets without fully unwinding the position.

Yields in tokenized private credit typically range from 8–15%, reflecting the credit risk and illiquidity premium relative to government debt — a spread wide enough to attract capital that finds Treasuries uninspiring and crypto volatility intolerable.

That's a fundamentally different product. And the market priced it accordingly.

Source: DLResearch

Issuance Was Never the Point

The important shift wasn't that private credit got tokenized. It's that private credit became usable on-chain — and that distinction is everything.

Tokenization without utility is just digitized paperwork. There's a meaningful difference between an asset that lives on-chain and an asset that works on-chain. For most tokenized RWAs, the journey ends at the wallet — issued, held, and redeemed. Private credit went further and became collateral; it became something you could borrow against without exiting, legible to permissionless protocols that had no memory of what a loan originator was. That transition — from token to financial primitive — is the one that actually matters.

On-chain private credit outstanding reached almost 4$B by May 2026, up over 200% from $1.14B at the start of 2025, but the raw number undersells the structural shift. The more significant datapoint is where that capital sits: the majority of private credit active market cap on-chain is in permissionless products — open protocols where the asset behaves more like a crypto-native instrument than a traditional fund interest that moves once a quarter when redemptions open.

Users don't just want exposure to private credit, but they strive for private credit that works inside DeFi — transferable, financeable, usable across venues. Those are different demands, and the market is already separating the products that satisfy the first from the ones that satisfy both.

Capital Follows Utility, Not Packaging

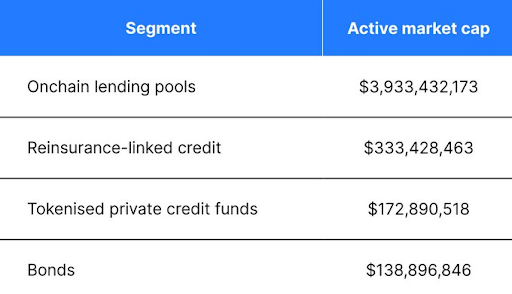

The largest share of on-chain private credit isn't sitting in tokenized fund wrappers. It's in on-chain lending pools — structures built for crypto rails from the ground up, not traditional products repackaged for new distribution channels.

Aave's RWA-focused money market Horizon surpassed $176M in loans outstanding, marking a credible institutional entry into tokenized private credit. Morpho, meanwhile, grew its loans outstanding from $1.9B to $3.0B, establishing itself as the second-largest lender on-chain — now operating across 29 chains versus Aave's 19. RWA.xyz These are not a tokenization platform, but DeFi lending protocols absorbing private credit as productive collateral. The asset has moved from issuance infrastructure into core DeFi plumbing.

Maple Finance CEO Sidney Powell has argued that as on-chain lending develops, crypto-backed loans will eventually receive ratings from traditional credit agencies — potentially by the end of 2026. Once rated, these instruments can be syndicated into mainstream fixed-income mandates, turning them from alternative assets into investment-grade instruments by conventional frameworks. That's the full arc: from niche DeFi yield to rated, institutionally allocated credit. Private credit is the only RWA category currently on that trajectory.

This is why the comparison to other categories is instructive. Real estate can be tokenized, but secondary liquidity and on-chain valuation remain unsolved. PE and VC can be wrapped, but they stay passive — there's no DeFi use case for a ten-year lockup. Both private credit and tokenization share a common goal of disintermediation: where private credit bypasses banks through direct lending, tokenization seeks to use smart contracts in place of financial intermediaries. They're philosophically aligned, and that alignment is part of why the integration has been smoother than with other asset classes. Private credit is one of the first categories where tokenization improved both access and active financial use simultaneously — and Keyrock estimates gradual growth of on-chain private credit to $15–17.5B by the end of 2026.

The Scale of What's Still Untouched

Here's the number that reframes the entire conversation: the global private credit market is valued at over $1.7 trillion these days.On-chain private credit, even at $12.9B, represents less than 1% of that total.

Cumulative on-chain private credit originations have reached $33.66B— meaning the total capital that has flowed through these structures is already multiples of what's currently outstanding. The pipes work, but the question is how fast the volume through them scales.

The regulatory layer is the honest constraint: Most leading pools in the US sit behind Reg D 506(c) or Reg S structures for non-US participants. In Europe, the EBA issued preliminary guidance in March 2026 on what tokenized credit originations require for capital treatment at bank counterparties. The direction of travel is toward clarity, but the pace still matters. Every quarter of regulatory ambiguity is a quarter where institutional capital that wants to allocate stays on the sidelines.

None of This Changes the Underlying Risk

The honest caveat, stated plainly: it's still private credit, because underwriting matters as well as the borrower quality and recovery rates. Tokenized private credit does not fix the underlying illiquidity of the loans, but makes it transparent, prices it in real time, and lets allocators trade exposure through secondary markets that run 24/7 on-chain. When a loan delinquency hits, the secondary price moves within minutes. That's a structural improvement over quarterly redemption windows with liquidity gates — the model that was forced into emergency backstops.

But transparency is not the same as safety. A poorly underwritten receivables book is still a poorly underwritten receivables book, regardless of which chain it settles on. The stress test hasn't arrived at scale yet. But when it does, the protocols that built a rigorous underwriting infrastructure will separate from those that built elegant token wrappers.

The Template for What Comes Next

Private credit's trajectory is the cleaner way to think about the rest of the RWA market — not as a series of asset classes waiting to be wrapped, but as a test of which assets become more useful once they're part of an on-chain financial system.

The category leaders in the next phase won't be the assets that are easiest to tokenize: the winners will produce real financial functionality from being on-chain, like new collateral types, new yield structures, and new ways to finance positions that didn't exist in the traditional system. Private credit passed that test first because its cash flow mechanics translated cleanly into DeFi primitives.

The question for every other RWA category — real estate, infrastructure debt, trade finance, royalties — is the same one private credit already answered: what does this asset actually do once it's on-chain that it couldn't do before?

The ones with a convincing answer to that question are the ones worth watching. The ones without one are just filing cabinets with better branding.

To learn more about private credit:

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.