The $100 Infrastructure Play:We’re Lowering the Threshold

Private credit has spent the better part of two decades being one of the most consistent return generators in institutional finance — and one of the most deliberately inaccessible asset classes ever constructed.

Serving smaller investors costs more than they generate, so the market didn't serve them. That logic has a shelf life, and it expires when the infrastructure changes.

The Number That Changes the Argument

The $3.2 trillion market has delivered yield stability, negotiated terms, and low correlation to public markets across economic cycles — with tokenized structures now offering 8–14% yields against public debt benchmarks that don't come close. Entry into the best deals has historically required minimum tickets of $250,000 to $1 million, lock-up periods measured in years, and a compliance apparatus that made the entire exercise impractical for anyone below a certain balance-sheet threshold.

The architecture was designed that way because the distribution infrastructure did. WisdomTree launched its Private Credit and Alternative Income Digital Fund with a minimum investment of $25, T+0 settlement for subscriptions, tokenized on Ethereum and Stellar, available to both retail and institutional investors.

Yes, you’ve got that right: $25 minimum in the private credit sector, coming from a $100 billion asset manager with a NYSE listing and decades of institutional credibility!

That figure is not a rounding error, but rather an arithmetic consequence of replacing a distribution infrastructure that charged 200–350 basis points in operational friction with a smart contract that doesn't distinguish between ticket sizes. The marginal cost of serving a $100 investor and a $1 million investor on tokenized rails is approximately the same. When the marginal cost collapses, the minimum viable ticket goes down drastically with it.

This is what most RWA commentary misses. The focus lands on yield numbers and market cap milestones, and what matters more is the directionality of the access threshold — and it is moving in one direction only.

What the Old Infrastructure Actually Cost

To understand why a $25 minimum represents a genuine structural break, it helps to be precise about what the old model charged. Let’s take a specific example.

Singapore investor accessing a Manila receivables facility through traditional rails would navigate custodian accounts across two jurisdictions, Bangko Sentral registration requirements, two FX conversion legs at 80–120 basis points each, SWIFT settlement threading through 2.3 correspondent intermediaries on average, and legal documentation requiring qualified counsel in both markets. Total friction: 200–350 basis points annually. On a 12% gross yield, survivable — but only at ticket sizes large enough that the drag didn't consume the return premium. Below the $500,000 line, the economics didn't close.

Previously, the people excluded by that threshold were mass-affluent investors, smaller family offices, and retail participants in emerging markets who lacked neither the judgment nor the interest — only the capital to clear the minimum. The number of on-chain RWA holders stood at over 750,00 as of early May 2026 — a figure that reflects institutional adoption rather than retail participation, given the minimum investment thresholds governing most regulated tokenized products. Those thresholds are now collapsing under the economics of a different settlement layer.

The Infrastructure Case

The IMF put it clearly in its April 2026 note on tokenized finance. Tokenization enables finer-grained ownership through fractionalization — and allows valuation, compliance checks, and cash flows to be automated via smart contracts, reducing operational complexity at every point in the stack. "Finer granularity of ownership" is, in practical terms, the elimination of the minimum ticket as a structural feature of the asset class.

The growth numbers reflect this as tokenized private credit rose 82% between year-end 2024 and October 2025 to $17.9 billion, while tokenized institutional alternative funds grew 749% over the same period to $2.97 billion. Capital is moving into structures that previously required institutional-scale entry, precisely because the entry threshold has started to move.

Morgan Stanley's wealth management division is now using blockchain to offer clients direct access to private equity, credit, and real estate through tokenized funds, managing digital and traditional assets through a single unified dashboard. Their clients are not the $25 minimum audience, but the infrastructure being built to serve them — portable fund ownership, programmable yield distribution, multi-chain settlement — is identical to the infrastructure that makes that minimum tickets viable. The institutional buildout and the retail access expansion are running on the same rails, where one subsidises the other.

The Yield Pickup

The access argument stands only if the yield justifies the reach. It does.

Tokenized private credit delivers 8–14% returns against public debt benchmarks, with on-chain infrastructure enabling continuous secondary-market pricing around the clock. When a pool weakens, token prices recalibrate within minutes, and not through quarterly redemption gates. Sellers seeking liquidity meet buyers hunting discounted exposure. No gates or NAV theatric with board deliberations over withdrawal limits.

The spread reveals the mechanism at work. US 10-year Treasuries yield 4.2% as of early May 2026. Investment-grade SGD corporate credit trades at 4.5–5.5% for a two-to-three-year duration. The gulf between those benchmarks and 10–14% private credit returns doesn't map to proportionally higher risk, but it maps to access friction being structurally unwound. As that friction dissolves, spreads will narrow. The window for capturing friction-priced yield is finite, and it closes faster than consensus expects.

Where This Lands

The WisdomTree $25 minimum describes a direction, not an endpoint. The managers, fintechs, and platforms building tokenized credit infrastructure are not doing so to serve investors who already have access. Fact is, the investors who don't have access represent an order of magnitude more capital in aggregate, and the technology has removed the excuse for not reaching them.

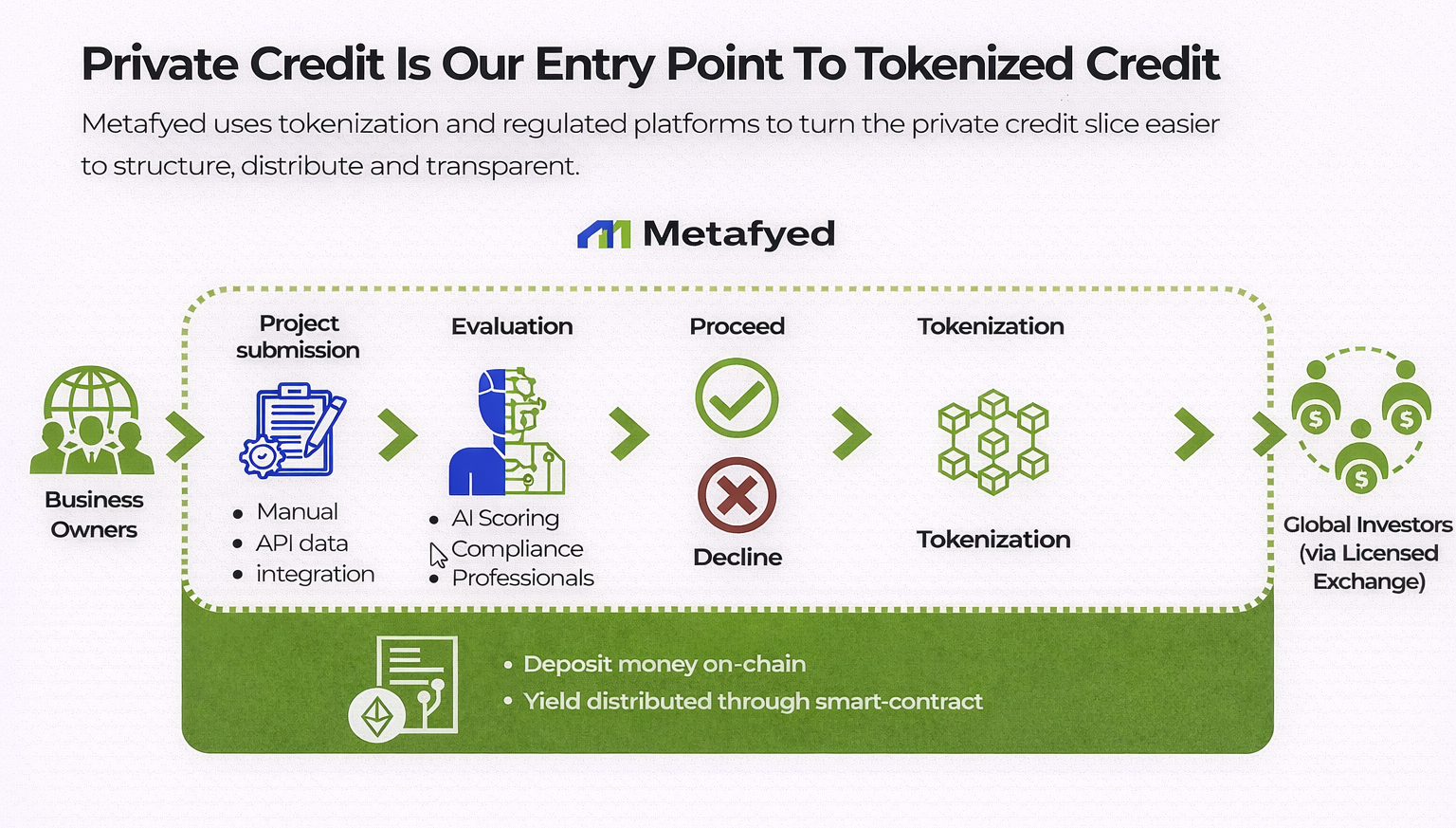

Metafyed was built on exactly this premise: that the access threshold to institutional-quality private credit in Southeast Asia was a cost issue dressed up as a risk problem. A Singapore investor accessing a Manila receivables deal yielding 12% through on-chain infrastructure completes onboarding in hours, settles atomically, and receives monthly yield distributions automatically without the custodian accounts, the FX legs, or the bilateral legal agreements. The $100 minimum ticket is the natural output of infrastructure that doesn't charge for intermediation it has replaced.

The $25 WisdomTree minimum and the $100 Metafyed threshold are different numbers pointing at the same reality: the floor on who gets to access institutional-quality yield is falling. It fell because the infrastructure changed, and it will keep falling for the same reason.

An asset class that spent two decades monetizing scarcity is discovering that access, once abundant, ceases to be merchandise.

Learn more at:

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.