The Key Trends Defining Tokenization in 2026

What began as pilots is now reshaping capital markets by rebuilding how financial instruments are issued, settled, and owned globally. If 2024 was the year tokenization became credible, and 2025 was the year it became institutional, then 2026 is the year it becomes the default.

At Metafyed, we've been watching this shift up close, and what's happening this year is no longer a trend. Let’s examine the key defining directions in the RWA sector together.

Catching The Wind Of Change

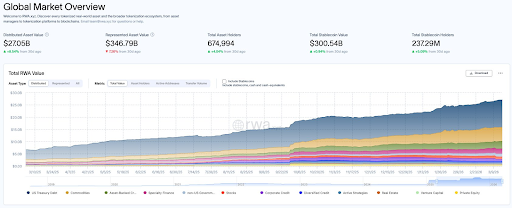

The numbers are quite unambiguous: according to RWA.xyz, the total value of on-chain real-world assets surpassed $20 billion in early 2026, excluding stablecoins, and that’s more than double the $8 billion recorded at the start of 2025.

What is invigorating here is the fact that it’s not a speculative capital chasing a narrative. We witness the inflow of institutional money moving into tokenized assets because the infrastructure is mature, and the regulatory frameworks are finally catching up.

What's changed is the convergence of three things that had to arrive together: regulatory clarity, institutional-grade custody, and platforms that have quietly solved the hardest problems: compliance automation, cross-chain interoperability, and secondary liquidity.

At Metafyed, we built for exactly this very moment. Tokenization is no longer a proof of concept, slowly becoming the operating layer through which real capital moves — and the businesses and investors who understand that now are the ones who will be best positioned for what comes next.

Accoording to RWA.xyz data

1. Private Credit Is the Breakout Asset Class of 2026

While real estate captured the early imagination of the tokenization narrative, private credit is where the serious volume is being built right now. Global private credit assets under management surpassed $2.1 trillion in 2025, according toPreqin, and a growing share of new issuances are exploring on-chain distribution as a core component — not an afterthought anymore.

The reason is structural elegance. A private loan facility is fundamentally a contractual cash flow with interest payments, defined maturities, and predictable risk parameters. That structure maps almost perfectly into a smart contract: tokenizing a credit instrument is a cleaner technical and legal exercise than tokenizing a physical building, and the yield profile — typically 8 to 12 percent net in senior-secured private credit is exactly what a rate-sensitive investor market is hungry for.

Platforms likeMaple Finance and Centrifuge have demonstrated this at scale, collectively facilitating hundreds of millions in on-chain credit. What's accelerating in 2026 is the move from crypto-native borrowers to real-economy borrowers — SMEs, infrastructure developers, trade finance operators — accessing tokenized credit rails for the first time.

2. Institutions Have Stopped Piloting and Started Deploying

The single most important signal in the market right now is the shift from institutional experimentation to institutional commitment.BlackRock's BUIDL fund, a tokenized money market fund launched on Ethereum in 2024, crossed $1 billion in assets under management within months of launch, making it the largest tokenized treasury fund in existence. Franklin Templeton's BENJI token is live across multiple blockchains. Standard Chartered has an active tokenization desk, and HSBC tokenized gold through its Orion platform.

These are product lines, and what has enabled this shift is the maturation of the legal and custodial layer. Qualified custodians — like Anchorage Digital, Fireblocks, Komainu — now hold tokenized securities with the same institutional-grade safeguards as traditional assets. Legal opinions on the enforceability of smart contract ownership have been standardized across key jurisdictions. Now, capital is flowing.

3. Regulatory Frameworks Are Hardening Into Competitive Advantage

For years, regulatory ambiguity was the single greatest brake on institutional participation. That is changing fast, and the geography of where it's changing matters enormously.

The EU's Markets in Crypto-Assets regulation (MiCA), now fully in effect, has created a passportable compliance framework across 27 member states. Singapore's MAS Project Guardian, a cross-industry initiative involving JPMorgan, DBS, and Standard Chartered, has produced live tokenized bond and fund pilots with real regulatory backing. Next, Hong Kong's SFC has licensed multiple tokenized securities platforms and is actively positioning the city as Asia's tokenized asset hub. Moreover, the UAE's ADGM and DIFC have created some of the most permissive and well-structured digital asset frameworks in the world.

The pattern is consistent: jurisdictions that move early on clear frameworks are attracting issuers, platforms, and capital. Regulation is no longer a headwind, as in the right markets, it is becoming a moat.

4. On-Chain Compliance Is Making the Back Office Obsolete

One of the quietest but most consequential shifts in 2026 is the maturation of programmable compliance. Novel token standards allow issuers to embed KYC, whitelisting, transfer restrictions, jurisdictional caps, holding period enforcement, and investor accreditation rules directly into the token itself.

This means the asset is compliant by architecture, and there is no transfer agent manually checking an eligibility list or a fund administrator processing redemption requests at the end of the month. The smart contract enforces the rules in real time, every time, with a complete and auditable on-chain record.

For mid-market issuers, such as the businesses that have historically been priced out of professional fund structures because of administrative overhead, this is quite transformative. The fixed cost of a compliant token issuance is now a fraction of what a traditional private placement costs, and the ongoing operational burden is dramatically lower.

5. Interoperability Is Unlocking Real Liquidity

The early tokenization ecosystem suffered from a critical flaw: liquidity fragmentation. A token issued on Ethereum couldn't interact with a buyer on Avalanche. A fund on Stellar couldn't accept capital from Polygon. Each chain was an island, and these isolated islands didn't have liquid markets.

That is being systematically resolved. Cross-chain messaging protocols — like Chainlink's CCIP, LayerZero, Axelar — are enabling tokenized assets to move across chains with the same compliance controls intact. Institutional networks are creating interoperable, privacy-preserving rails that connect bank ledgers with public blockchains.

The result is that a tokenized private credit note issued in Singapore can now be visible, purchaseable, and settleable by an investor in Dubai using infrastructure that didn't exist 18 months ago. When liquidity connects, valuations improve, and more issuers start to tokenize. So, the flywheel is turning.

6. Retail Access Is Arriving — and It's More Serious Than the Last Cycle

This is not something like the 2021 hype-driven market or the 2017 ICO-fueled wave. The retail tokenization products launching in 2026 are regulated, custodied, and built on real underlying assets generating real yield. Platforms operating in MiCA-compliant jurisdictions and under MAS frameworks are offering fractional access to private credit and infrastructure assets with minimum investments as low as $500 to $1,000 — a category that simply did not exist for these asset classes before.

The mass-affluent investor segment across Southeast Asia alone represents an addressable market in the hundreds of billions. Indonesia, Vietnam, and the Philippines collectively have tens of millions of investors with savings capital and a chronic shortage of yield-bearing, regulated investment products. Tokenization is not pitching them a new technology, but rather delivering a financial product they already want, through infrastructure they already use.

7. Tokenized Yield Is Redefining What a Savings Product Looks Like

Perhaps one of the most structurally significant developments of 2026 is the convergence of dollar stability and on-chain yield. Products that combine USD-pegged value with yield generated from tokenized T-bills, money market funds, or private credit are collapsing the distinction between a stablecoin and an investment product.

For investors in emerging markets — who want dollar exposure, capital preservation, and yield simultaneously — this convergence is not a nice-to-have. Consider this to be a better savings account. The industry projects have already demonstrated that on-chain, yield-bearing dollar instruments have real, sustained demand. In 2026, that model is being extended to higher-yielding private credit and real asset collateral, pushing net yields into ranges that traditional savings infrastructure can’t touch.

The Takeaway: Where Are We Heading?

The tokenization market in 2026 isn’t defined by a single trend, but several structural forces arriving at the same time, reinforcing each other. And retail access is finally arriving on terms that are regulated, transparent, and built on real yield.

The opportunity window for platforms, issuers, and investors who move now is significant because the infrastructure is finally complete enough to support scale. The market is moving fast, and the only scarce resource left is positioning.

Get ahead of the curve with Metafyed. Learn more:

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.