From Pilot to Pipeline:Diversifying Beyond Crypto in 2026

Private credit is one of the oldest forms of lending in the world, and one of the newest asset classes to arrive on-chain. Businesses have borrowed outside the banking system for centuries. Now, we face a different landscape that is changing fast, and with that come many lucrative opportunities that were previously inaccessible to retailers.

What Is Private Credit? Start Here.

However, private credit as a structured asset class, with dedicated funds, institutional capital, and formal underwriting, is a product of the last 40 years, as the first companies were incorporated in the 1980s.

The post-COVID era of 2022–2025 accelerated the model into what many now call its Golden Age. Private credit is, at its most basic, lending that happens outside the traditional banking system. Instead of a company borrowing from a bank, it borrows directly from an investor or a fund — in exchange for a structured return, typically interest payments over a fixed term.

The “private” in private credit refers to the fact that these loans are not publicly traded on an exchange. They are negotiated directly between the borrower and lender, structured to fit specific needs, and held to maturity. That directness is both the source of the yield premium and, historically, the reason retail investors have been locked out.

Private credit sits alongside private equity and venture capital as part of the broader alternative assets universe. But unlike equity, where returns depend on a company's growth, private credit is structured as debt: the borrower pays a fixed or floating rate, and the lender's return is contractual.

"Private credit is doing exactly what investors hoped it would: providing strong, floating-rate yield and acting as a shock absorber from market volatility." —KKR, Private Credit Outlook, October 2025

The Numbers: A $3 Trillion Market on Its Way to $5 Trillion

The market stood at $3 trillion in 2025, up from $2 trillion in 2020, according toMorgan Stanley's Private Credit Outlook. And it is estimated to reach $5 trillion by 2029, driven by bank retrenchment, institutional demand for yield, and the structural financing needs of a global economy that has outgrown traditional lending channels.

Currently, 76% of private credit AUM is held by institutional investors — predominantly pension funds, insurance companies, and sovereign wealth managers, perAIMA's 2025 Private Credit Report. The remaining 24% held by retail and mass-affluent investors is growing, but access has remained constrained by structural barriers that tokenization is now dismantling.

The firms deploying capital at scale read like a who's who of global finance: Apollo, Blackstone, Ares, BlackRock, KKR, Carlyle. JP Morgan earmarked $50 billion for direct lending, while Goldman Sachs raised over $20 billion for private credit strategies. This is no longer a niche product as it has become the asset class that institutional capital has rotated into as public market yields have compressed.

Why Private Credit Yields So Much More

The yield premium — typically 10–15% for institutional investors, and 15–20% for Asian private credit via platforms like Metafyed — comes from four structural sources:

Illiquidity premium. Private credit is not tradable on a public exchange. Investors accept that capital is locked for the duration of the loan, and, in exchange, they receive a higher rate than a comparable publicly traded instrument.

Complexity premium. Private credit deals require significant due diligence, legal structuring, and ongoing monitoring. That effort commands a fee, and tokenization reduces this cost substantially without eliminating the premium.

Bank disintermediation. As banks have retreated from certain lending markets — driven by Basel III/IV capital requirements and post-GFC risk aversion — private credit has filled the gap. Structural demand from borrowers who have no other source of capital supports higher rates.

Emerging market premium. In Asia specifically, underdeveloped credit markets, strong underlying demand, and limited competition create a meaningful additional yield layer above Western private credit benchmarks.

The Legacy Business Behind the Token

When Metafyed tokenizes a private credit deal, the token represents a legal claim on the cash flows of a real, operating lending business.

For example, pawn lending is one of Asia's oldest and most resilient credit models. Borrowers pledge physical assets — such as jewellery, electronics, luxury goods — against short-term loans. Recovery rates are high because the lender holds physical collateral. The business has operated profitably through financial crises, recessions, and pandemics.

These are established, cash-generating lending businesses with years of operating history, known default profiles, and asset-backed collateral structures. Tokenization does not alter the underlying economics but instead changes who can access them.

"The token is not the asset. The token is the key that unlocks access to the very asset. The asset has been there for decades — paying returns that only institutions could reach."

What “On-Chain” Actually Adds

While the “on-chain” has become a buzzword during the last few years, there’s a definitive and quantifiable value that sits behind that definition. However, what does it mean for lending markets?

Fractional access. A pawn lending book that previously required a $250,000 minimum can be divided into tokens at any denomination. Metafyed's exchange partners have processed allocations from much smaller amounts. The underlying yield and security structure are identical to what an institutional investor receives.

Exchange liquidity. Metafyed distributes through NXMarketin, the Philippines, and NexStox in Malaysia — regulated exchanges where tokens are listed and tradeable. This creates a secondary market pathway that traditional private credit has never had.

Transparent settlement. Every distribution, like a coupon payment, every principal repayment is executed via a smart contract. No fund administrator calculating NAV or quarterly PDF here. The on-chain record is the only record.

Anchor underwriting. Metafyed's strategic investors commit 50–60% of every deal before it goes public. When a sophisticated institutional partner has already subscribed to the majority of the deal at the same terms being offered to retail, the quality signal is embedded in the structure itself.

The Risk Landscape: What Investors Need to Know

The honest summary: private credit yields more because it requires more patience, due diligence, and risk tolerance. Yes, several factors need to be considered before entering this sector:

Credit risk. The borrower may not repay. Metafyed's mitigation is threefold: AI-powered due diligence scoring before any deal reaches investors, anchor underwriting, and asset-backed collateral structures in the underlying loan books.

Liquidity risk. Exchange listing creates a secondary market, but thin trading volumes in early-stage markets are a reality. Investors should treat these as medium-term commitments and not short-term instruments.

Regulatory risk. The tokenized securities landscape is evolving. Hong Kong's SFC and Malaysia's SC are actively building frameworks for digital asset securities. Metafyed operates exclusively through licensed exchange partners to stay within regulated parameters as those frameworks develop.

The argument for tokenized private credit is not that those risks disappear. It is that, for the first time, the risk-adjusted return profile that institutions have assessed for decades is now available to investors who previously had no route in.

The Metafyed Thesis in Plain Terms

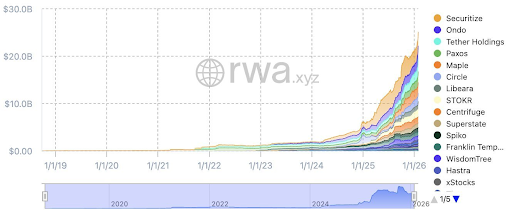

The tokenized RWA market has surpassed $25 billion in on-chain value as of early 2026, per Nexo's RWA tracker. Private credit is the largest non-stablecoin category in that market — and Asia, with its structural financing gap and fast-moving regulatory environment, is where the most compelling deals are being originated.

What’s more important, private credit is already the asset class of the decade. The institutional consensus is clear: private credit is the most compelling risk-adjusted yield available in a world of compressed public market returns.

And what has been missing is access: the minimum tickets, the regulatory barriers, and the back-office complexity — these have kept private credit as an institutional product for the last forty years.

Metafyed's position is straightforward: lending businesses exist along with yields. What we are building is the tokenization layer that makes it possible for a verified investor anywhere in the world — with any amount of capital — to access the same deal that a family office in Singapore would.

The legacy business is already on-chain. Are you looking to get on board and invest in tokenized Asian private credit? Ask us how.

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.