Private Credit 101:Why Institutions Love It, and Why It's Going On-Chain

The private credit market is projected to reach $5 trillion by 2029 and quietly become one of the most consequential asset classes in global markets, financing everything from mid-market manufacturers in Southeast Asia to AI data center buildouts across the United States. 94 percent of institutional investors now allocate to it, but the average retail investor in Asia holds zero exposure. That gap is not a coincidence. Why?

That barrier was deliberately engineered into the asset class from inception. Tokenization is the first mechanism powerful enough to dismantle it permanently. Metafyed is building the gateway that lets regular investors into private credit markets — a world the wealthy have kept to themselves until now.

What Private Credit Actually Is

Let’s strip away the jargon, and private credit is straightforward: Private credit is direct lending that happens outside public bond markets and outside bank balance sheets. When a mid-market business needs capital and banks are too slow, too constrained by Basel III capital requirements, or simply uninterested in a deal below their threshold, it turns to a private credit fund. The fund lends directly, negotiates terms bilaterally, and holds the loan to maturity without syndication, public rating, or a daily mark-to-market. Just a borrower, a lender, and a contract are needed for this equation to work.

Direct lending — private credit funds making loans directly to companies — accounts for close to 60 percent of total private credit activity nowadays. But the asset class extends well beyond direct loans. It includes trade finance — lending against invoices and receivables from verified commercial counterparties, asset-backed finance — lending secured against specific pools of assets like equipment, inventory, or real estate. Mezzanine debt — junior capital sitting between senior debt and equity in a borrower's capital structure, carrying a higher yield to compensate for lower seniority. And specialty finance — everything from litigation funding to royalty streams to infrastructure debt.

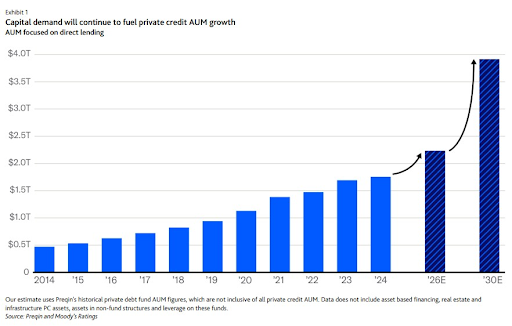

Today, the addressable market for private credit is upwards of $40 trillion, most of it investment grade. What has been captured so far — the $3 trillion in AUM — represents a fraction of what exists. The middle market alone is made up of nearly 200,000 companies that represent one-third of private sector GDP and would rank as the fourth largest economy in the world behind the US, China, and Japan. These businesses need capital, and banks are retreating from serving them. They are creditworthy borrowers who have been underserved by a banking system that retreated from their segment after 2008 and never fully returned. Private credit filled that vacuum. The investors who provided the capital have been collecting the premium ever since.

Why Institutions Have Been Quietly Compounding on This for Two Decades

The institutional love affair with private credit comes down to four structural advantages that public fixed income has never consistently replicated. Four structural advantages explain the institutional allocation to private credit — advantages that public fixed income has never consistently replicated.

1) Yield. During seven periods of rising rates since 2008, direct lending averaged 11.6 percent returns — two percentage points above its own long-term average. Private credit has sustained approximately 200 basis points of premium over leveraged loans and high-yield bonds across market cycles. That premium is the illiquidity premium — the return an investor earns for accepting a lock-up rather than daily liquidity. It is not compensation for higher credit risk. It is compensation for a structural constraint that institutional investors, with their long-dated liabilities, are uniquely positioned to absorb. Direct lending posted a 10.5 percent annualized return in Q4 2024 — beating high-yield bonds and leveraged loans even as the Federal Reserve was cutting rates.

2) Seniority. Most private credit sits at the top of a borrower's capital structure — senior secured, with specific assets pledged as collateral. In a liquidation, senior secured lenders are first in line. Blackstone's direct lending strategy has maintained a 0.08 percent annualized loss rate over 20 years.That figure is not a product of exceptional managerial skill, but rather the mathematical output of lending at the top of the capital stack with enforceable collateral underneath every position.

3) Floating rate protection. Private credit loans typically carry floating-rate coupons that adjust with benchmark rates, providing real-time interest rate protection that fixed-rate bonds cannot offer. Between 2022 and 2024, when central banks across developed markets raised rates at the fastest pace in four decades, private credit investors earned more on every basis point of tightening. The instrument is structurally long rates in a rising environment — the opposite of the duration exposure that decimated public bond portfolios in the same period.

4) Low correlation. Private credit tends to be less sensitive to day-to-day market swings, helping diversify portfolios beyond traditional asset classes. During the 2022 simultaneous selloff in both equities and bonds — the worst year for the 60/40 portfolio in decades — private credit continued generating contractual yield. Cash flows respond to borrower obligations, not to market sentiment. In a diversified portfolio, that independence has a value that only becomes fully visible when everything else is falling simultaneously.

JP Morgan recommends private credit at approximately 15 percent of a core private markets allocation — translating to 1.5 to 4.5 percent of overall portfolios — balancing direct lending with asset-backed finance and opportunistic credit. The world's largest pension funds, sovereign wealth funds, and insurance companies have been building these allocations for years, so the results compound silently inside institutional portfolios. Retail investors in Asia watch from the outside.

The Access Problem — Built In, Not Accidental

The structural exclusion of retail investors from private credit is not a regulatory artifact or an oversight. This is the direct consequence of how the asset class was designed to operate.

Minimum ticket sizes at leading private credit managers — likeAres Management,Blue Owl Capital,Blackstone Credit — start at $500,000 for individual investors and frequently require $5 million or more for access to top-tier strategies. Meanwhile, institutional funds may require minimum investments ranging from $250,000 to several million dollars.That filter eliminates the overwhelming majority of investors in Asia, regardless of sophistication.

Lock-up periods compound the problem: most private credit funds have lock-ups between three and seven years due to illiquid loan structures.Top1000funds For an investor without a multi-million dollar portfolio to draw liquidity from elsewhere, that commitment is practically impossible to make. The asset class is not unsuitable for retail investors — the risk profile of a senior-secured loan is more conservative than most public equity exposure. The lock-up is an operational convenience for fund managers, not a risk management necessity for the investor.

Distribution infrastructure is the third wall. Private credit funds are distributed exclusively through private banks, family offices, and institutional placement agents. They do not appear on the retail brokerage platforms or digital investment apps that most Asian investors actually use. The investor base for private credit remains predominantly institutional, accounting for 76 percent of private credit AUM. The share held by retail and mass-affluent investors — 24 percent — is expected to grow. That growth is being driven by tokenization, not by any relaxation of traditional distribution gatekeepers.

Why Tokenization Changes the Math

Tokenization does not change what private credit is: The loan is still a loan, the borrower still pays interest, and the collateral is still being pledged. Finally, the legal obligation is still contractual and enforceable. What tokenization changes is the wrapper around those instruments — and that wrapper is responsible for every barrier that has kept retail investors out.

When a private credit facility is tokenized, the legal ownership of a fractional interest is represented as a digital token on a blockchain, and that token can be issued in denominations starting at only $100. The minimum ticket disappears because the marginal cost of onboarding a $100 investor and a $500,000 investor through blockchain infrastructure is essentially identical. The economic rationale for the minimum never applied to the underlying asset, but to the administrative cost of the old wrapper. The new wrapper eliminates that cost.

Assets held in evergreen private credit funds reached $644 billion as of June 2025, up 28 percent from the end of 2024 and roughly 45 percent year-over-year. A significant portion of that growth is being driven by semi-liquid structures that offer retail and mass-affluent investors access to private credit with reduced lock-up constraints. Tokenization takes that structural evolution further — secondary transferability of tokens means liquidity is a market function, not a fund administrator's discretionary decision.

The compliance infrastructure that previously required a team of lawyers and fund administrators runs automatically, reducing the cost of a compliant issuance from hundreds of thousands of dollars to a fraction of that cost, and the resulting reduction flows directly into accessible entry points and wider distribution.

Blue Owl Capital In Asia, equivalent regulatory momentum is building across Singapore's MAS framework, Hong Kong's SFC licensing of tokenized securities platforms, and the UAE's ADGM digital asset regulations. The direction is consistent: regulators are creating frameworks for retail access to private credit, and tokenization is the infrastructure that makes that access operationally viable.

At Metafyed, this is precisely the gap we are built to close. Private credit is not a niche product for sophisticated allocators, but this asset class has been artificially restricted by a distribution infrastructure designed for a world without blockchain. That world is changing: the investors who understand what private credit actually is — and what backs a tokenized interest in it — are the ones who will be positioned to capture the returns that institutional portfolios have been compounding in silence for two decades.

The New Gateway

Private credit's appeal to institutions is not complicated: contractual yield, collateral protection, floating rate structure, and low correlation to public markets. The market has grown from $2 trillion to $3 trillion in five years. Investors driving that growth are not taking outsized risk: they are accessing a structural premium that retail investors have been excluded from — because the wrapper around it was never designed to include them.

Tokenization redesigns the wrapper. The asset stays the same as well as the yield, and collateral stays the same. The only thing that changes is who gets to participate — and that change is permanent.

Looking for an easier pathway into private credit? Ask us:

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.