What Is Private Credit In 2026 And Why Is It the Quiet Engine of the Global Economy?

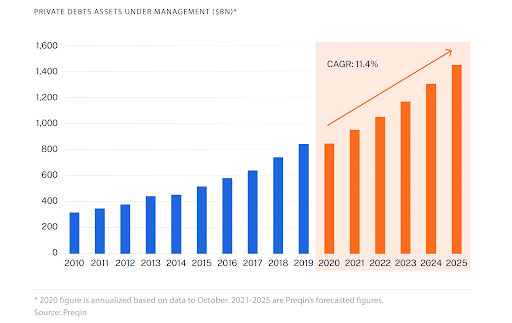

Private credit is an asset class that outperformed public bonds at nearly every rate environment over the last ten years, worth approximately $3.5 trillion as of early 2026, and is estimated to grow to approximately $5 trillion by 2029.

The tide is turning: until very recently, it was effectively invisible to anyone who didn't manage at least eight figures of capital. The potential is huge, but first, it's worth understanding exactly what private credit is — and why institutions have been so reluctant to share it.

What Private Credit Actually Is

Nowadays, 94% of institutional investors allocate to private credit, with institutional targets averaging around 8 percent of the total portfolio, while the average retail investor in Southeast Asia allocates zero. What is the reason for such a tremendous gap? That’s not a reflection of risk appetite or financial sophistication. This is a problem of access, and it has been one of the most quietly consequential inequalities in global finance for the past two decades.

Private credit is lending that happens outside the public bond market and traditional bank balance sheets. When a mid-market company needs $50 million to fund an acquisition, expand operations, or bridge a financing gap, it has two options: go to a bank or go to a private credit fund.

Banks, constrained by Basel III capital requirements and increasingly risk-averse after successive financial crises, have been retreating from mid-market lending for years. Private credit funds have stepped into that vacuum as they lend directly to businesses — hence the term "direct lending," the largest sub-category of private credit — and in exchange for the illiquidity and due diligence burden, they charge more. Significantly more.

The instruments themselves take several forms: direct loans to operating companies, mezzanine debt that sits between senior debt and equity in a capital structure, and asset-backed lending secured against receivables, inventory, or real estate. Next, there’s a specialty finance covering everything from litigation funding to royalty streams.

Each carries a different risk profile, but all share the same foundational characteristic: they are negotiated privately, held to maturity, and generate contractual cash flows in the form of interest payments.

And that last part — contractual cash flows — is the key to understanding why institutions love this asset class so much. But the time to disrupt the institutional monopoly has come.

Why Institutions Have Been Hoarding It

Private credit has delivered net returns of between 8 and 12 percent annually in senior-secured strategies over the last decade, according toPreqin. Investment-grade public bonds over the same period delivered 2 to 4 percent in most developed markets.

The gap is, however, structural, and it is persistent. The reason is the illiquidity premium. Simply: when you commit capital to a private credit fund, that money is locked up: you can’t redeem it next quarter or sell it on an exchange if sentiment shifts. In exchange for accepting that constraint, you earn a premium that public market investors simply don’t receive.

Institutional investors such as pension funds, sovereign wealth funds, insurance companies, and university endowments can absorb that illiquidity because their liability profiles are long-dated. A pension fund paying out benefits in 20 years doesn’t really need the flexibility that a retail investor theoretically does. So they allocate heavily, capture the premium, and compound it over decades.

Let’s provide a specific example: the California Public Employees' Retirement System— CalPERS — has a target allocation of 8 percent to private credit. TheAbu Dhabi Investment Authority allocates across the entire private credit spectrum. Blackstone's private credit platform manages over $300 billion.

These are not fringe allocations. Private credit has always been a core institutional asset class, generating returns that pension beneficiaries depend on, while the investors whose retirement savings fund those pensions have no direct exposure to the same instruments.

Why Retail Investors Have Been Locked Out

What’s worth noting: this exclusion was never accidental, and it operates through three specific mechanisms.

First, minimum ticket sizes. Most private credit funds require minimum commitments of $500,000 to $1 million for individual investors, and $5 million or more for institutional access to the best managers. That immediately eliminates the overwhelming majority of investors globally, regardless of their sophistication or risk appetite.

Second, lock-up periods. Private credit funds typically lock capital for five to seven years with limited redemption windows. For an investor without a multi-million-dollar portfolio to draw liquidity from elsewhere, that commitment is practically impossible.

Third, distribution gatekeepers. Private credit funds are distributed through private banks, family offices, and institutional placement agents — not through the platforms and brokers that most retail investors actually use. If your broker doesn't have a relationship with the fund manager, you simply never hear about the product.

The endgame result is a market where the best-performing asset class in fixed income is systematically inaccessible to the investors who would benefit most from its yield and diversification properties. In Asia specifically — where mass-affluent investors are accumulating capital at a faster rate than almost anywhere else in the world, but where alternative investment infrastructure remains thin — that exclusion is particularly sharp.

What Tokenization Does to Each of Those Three Barriers

Tokenization does not change what private credit is at the core: the loan is still a loan, and the borrower still pays interest. Moreover, the collateral is still real. What tokenization changes is the wrapper — but that wrapper is responsible for all three barriers.

When a private credit facility is tokenized, legal ownership of a fractional interest in that facility is represented as a digital token on a blockchain. That token can be issued in denominations as small as $500. The minimum ticket problem dissolves on the spot.

Because tokens are transferable on a secondary market, the lock-up problem becomes a liquidity management problem rather than an absolute constraint. An investor who needs capital in year three of a five-year facility can sell their tokens to another investor rather than waiting for maturity. Secondary liquidity in tokenized credit is still developing — it is not yet as deep as public bond markets — but the structural mechanism exists in a way it never did for traditional private fund interests.

And because tokenized assets can be distributed through digital platforms to any investor who passes KYC and accreditation checks, the gatekeeper problem collapses entirely. A verified investor in Jakarta or Ho Chi Minh City can access the same instrument as an elite investor in Geneva back in the days — through the same platform, at the same terms, with the same on-chain transparency into the underlying asset.

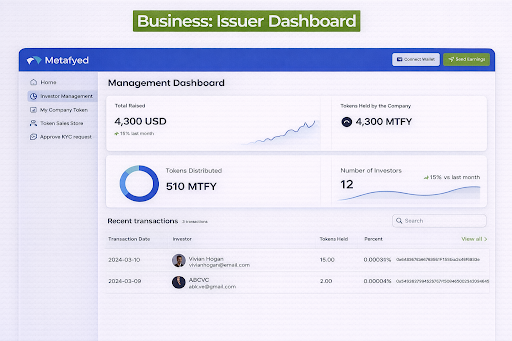

At Metafyed, this is the specific problem we are solving: private credit is not a niche product for sophisticated investors anymore. In 2026, think of it as a mainstream asset class that has been artificially restricted by distribution infrastructure. Tokenization removes that restriction.

Explore the lucrative possibilities of RWA investments at metafyed.com

Explore the lucrative possibilities of RWA investments at metafyed.com

Where This Leaves the Asian Investor Right Now

The mass-affluent investor in Asia is in a genuinely unusual position in 2026. Capital is accumulating faster than local investment infrastructure can absorb it.

While public equity markets are volatile, savings rates at domestic banks are real-return negative in most markets when inflation is accounted for. And yet one of the most consistently performing fixed-income asset classes in the world has been sitting just out of reach.

That reach is shortening now: regulated tokenized private credit products are live, the custody infrastructure is institutional-grade, and the legal frameworks in Singapore, Hong Kong, and the ASEAN countries have matured enough that sophisticated investors are allocating with confidence.

Private credit has been the quiet engine of global institutional portfolios for decades. On-chain finance is no longer the privilege of the few — it's a right for the many. A new financial frontier unfolds, and for the first time, it belongs to all of us. Start exploring it with Metafyed!

Explore how Metafyed is rebuilding Private Credit:

Visit our website I Follow us on X I Join the Telegram Community