Going Beyond the Wrapper: The Market Is Scaling Faster Than It Is Maturing

There is a version of the tokenization story where over $320 billion in tracked value means the worth of financial infrastructure has moved on-chain. Pantera Capital spent three months scoring 542 tokenized assets to find out whether that version is true.

It isn't: 3 in 4 tokenized assets are wrappers — and blockchain addresses attached to financial processes that haven't changed. The number got bigger, but the infrastructure mostly didn't. Those are different things, and the market has been treating them as the same one for long enough that the correction is overdue.

The Actual Shape of the Market

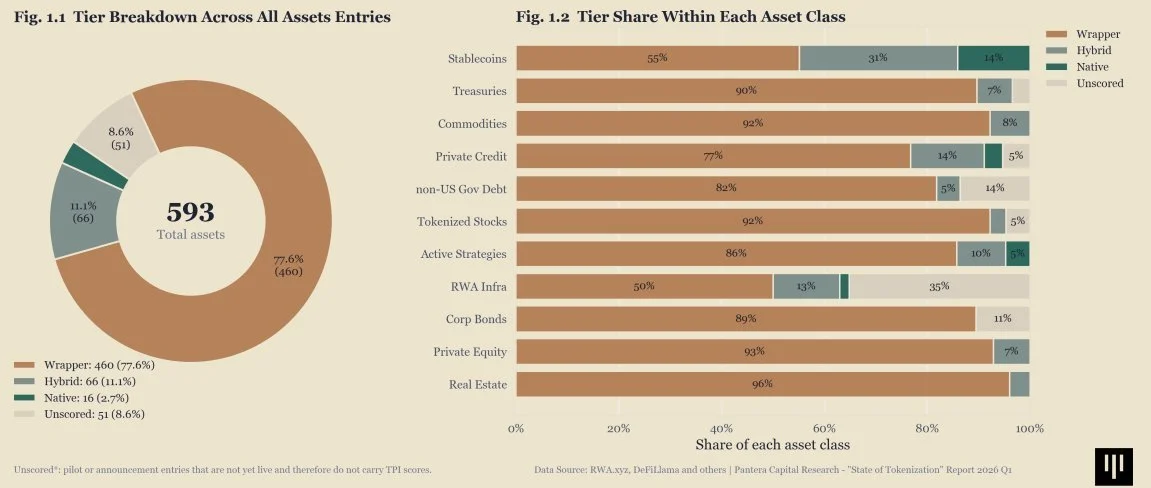

So, what’s this story all about? In a groundbreaking research, Pantera scored 542 tokenized assets on a scale from wrapper, where a token represents a claim on an off-chain asset held by a custodian, to native, where issuance, redemption, and custody all happen fully on-chain. The study found 77.6% of assets fell into the wrapper category. Only 11.1% were hybrid, and just 2.7% reached native status.

Those numbers describe the market more accurately than any AUM figure. In fact, 3 in 4 tokenized assets turned out to be digital receipts or claims on processes that still run almost entirely off-chain! The token exists on the ledger. Issuance, redemption, custody, transfer permissions, pricing, investor access — all of it still leans on the same intermediaries, manual processes, and settlement windows that tokenization was supposed to replace.

Issuance scored worst across all categories at 1.82 out of 5. Pantera found that 91.1% of assets still rely on gated minting and custodian-mediated exits, while only 13 products support autonomous mint-and-burn! The issuance layer — the first thing that should move on-chain — has barely moved at all for the overwhelming majority of the market.

This is why headline growth can be real while on-chain autonomy stays low. The two metrics are measuring different things: one measures how much capital has been assigned to a blockchain address, while the other checks how much of the financial lifecycle that capital goes through actually runs on-chain. Right now, those numbers are deeply disconnected.

Source: Pantera Capital Q1 Research

Wrapper Is the Default — and the Problem

The wrapper model has a legitimate early use case: it lowers friction for institutional distribution, provides traditional investors with blockchain-based access to familiar instruments without requiring changes to their custody, compliance, or settlement workflows. For institutions moving cautiously, the wrapper is a viable first step.

The problem is when the first step becomes the destination itself. A tokenized fund that still processes subscriptions through a transfer agent, prices NAV weekly, gates redemptions quarterly, and uses the blockchain purely as a distribution register has not changed its financial architecture. What has become different is the marketing material. The token is on-chain, but the fund is still not.

The assets that scored poorly in Pantera's framework tend to share common traits: thin secondary markets, unclear regulatory treatment, and dependency on off-chain intermediaries that reintroduce the exact counterparty risk that blockchain is supposed to eliminate. The wrapper model doesn't just fail to deliver on tokenization's promise — but it actively reconstructs the failure modes it was supposed to solve, wrapped in the credibility of a blockchain address.

Hybrid Is Where the Real Transition Starts

The 11.1% of assets classified as hybrid are part of the market worth watching, because they're the only category actually working on it.

Hybrid means some of the lifecycle has migrated on-chain: transfer logic, settlement flows, yield accrual, parts of compliance, or access control. Not fully native, yes, but no longer just a wrapper. The on-chain component is doing real work — enforcing a rule, executing a payment, or clearing a position without an intermediary in the loop.

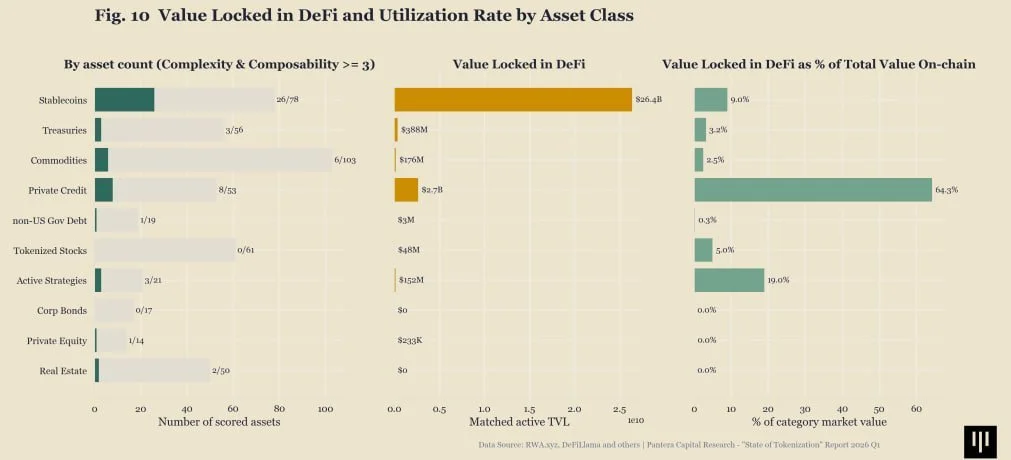

Private credit emerged as the standout non-stablecoin category for DeFi penetration, with 21.4% of value already active on-chain, ahead of actively-managed strategies at 19.6%. The reasons are structural, as private credit's cash flow mechanics — predictable yield, defined tenor, distributable interest — translate cleanly into smart contract logic. We are witnessing a rise in hybrid structures where a meaningful part of the financial lifecycle, such as yield distribution, position tracking, and secondary pricing, runs on-chain without custodian intermediation.

That is a qualitatively different product from a tokenized fund that sends monthly PDF statements and processes redemptions through a Cayman-domiciled administrator.

Source: Pantera Capital Q1 Research

Native Is Rare for a Reason

What’s interesting, only 55% of stablecoins were classified as wrappers — showing more maturity for the sector compared to other asset categories. Stablecoins are the clearest illustration of what native actually requires: USDC and USDT don't just exist on-chain, they operate there.

Getting to that standard for other asset classes is genuinely hard, as it requires moving not just the token but the operating model, like issuance and redemption logic, transfer enforcement, custody assumptions, and composability with other on-chain systems. Very few assets clear that bar because only a few issuers have rebuilt the operating model rather than just wrapping the existing one.

Stablecoins accounted for $293 billion, or 91.6% of total tracked value, and posted the highest average Tokenization Progress Index score. According to Pantera, stablecoins remain the only category combining real economic scale with measurable on-chain utility. Every other category is playing catch-up to an asset class that solved the native problem years ago — and the gap between stablecoins and the rest of the tokenization market is a measure of how much infrastructure work remains.

The Question That Actually Matters

Supply was never the constraint: 168 tokenized assets launched in 2025, up 115% from 2024 — the market has proven, at scale, that assets can go on-chain.

That question is closed now. The harder one is still actual: how much of the financial lifecycle moves with them? Issuance, redemption, custody, compliance, yield, transfer logic — the operational layer that separates a financial primitive from an expensive receipt. Mostly, it hasn't moved. The token went on-chain, while the infrastructure stayed put.

That's the real divide — not tokenized versus not, which describes a container, but distributed on-chain versus operating on-chain. The first is a marketing decision, and the second is architectural.

The market will price them differently, and the 77.6% in the wrapper tier will eventually face a blunt question: what do you offer beyond a blockchain address on a legacy structure? The next order of magnitude will come from that 2.7% who moved the operating model on-chain and proved it works.

Explore how Metafyed is doing tokenization the right way:

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.