The 2026 State of Onchain Credit: How a 225x Asset Class Is Rewiring Private Lending

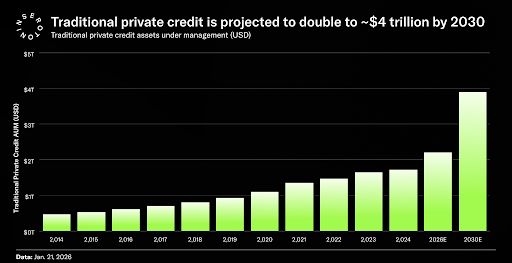

Private credit has been one of the most consistent return engines in institutional finance for two decades — averaging annualized returns north of 9%, growing from roughly $500 billion in assets under management in 2012 to $4 trillion globally by early 2026.

The growth has been relentless, the yields attractive, and the access deliberately restricted. Getting into the best private credit deals required a minimum ticket that excluded most of the investing world, a lock-up period measured in years, and a tolerance for quarterly redemption windows that a fund manager could close at will. That architecture is now being dismantled by on-chain infrastructure that is rebuilding the credit stack from the settlement layer up.

The Yield Problem That Onchain Credit Solves

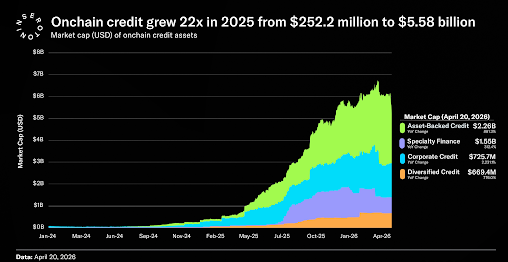

The numbers are no longer small enough to ignore. On-chain credit reached over $5 billion in distributed value as of May 2026, with private credit accounting for over $18 billion of the $36 billion tokenized RWA market when including represented value — making it the largest segment in tokenized real-world assets, bringing the total closer to $18-19 billion. This represents the most actively used category across DeFi, despite total on-chain RWAs (excluding stablecoins) growing from around $6 billion in early 2025 to more than $31 billion by May 2026.

On-chain credit introduces what practitioners call exogenous yield — returns generated by real-world lending activity, not by protocol token emissions or circular DeFi incentives. When a Maple Finance pool lends to a crypto trading firm, or a Centrifuge pool finances a portfolio of SME receivables, the yield comes from actual borrower interest payments on actual economic activity. That is a fundamentally different risk profile from liquidity mining rewards, and the market is increasingly pricing that distinction.

Yields vary by protocol and risk tier, offering 8% to 12%, depending on the underlying loan risk profile, reflecting country and borrower risks. Against a backdrop of 2.9% DeFi lending rates and 3.7% Treasury yields, that spread is the entire thesis.

Traditional private credit forecast

The Liquidity Architecture Advantage

The structural comparison to traditional private credit funds is where the on-chain model makes its clearest argument.

Blue Owl decided to sell $1.4 billion of assets, return capital to investors, and stop quarterly redemptions in one debt fund, while BlackRock limited withdrawals from a flagship debt fund, and Blackstone disclosed that BCRED faced first-quarter withdrawal requests equal to 7.9% of shares. These are not fringe events, but rather a redemption gate mechanism functioning as designed, placing the fund manager's liquidity management needs above the investor's exit preference.

Tokenized private credit provides continuous 24/7 secondary market pricing. When a pool experiences stress, the price of the token adjusts on the secondary market within minutes. Holders who need liquidity sell to buyers who want discounted exposure without the gate or a NAV-reset drama. The pool itself never has to sell assets; the liquidity happens around it, at the token layer, in public markets.

This is not a marginal improvement in user experience. What we face nowadays is a different liquidity architecture, with different risk distribution between fund managers and investors. And the market is beginning to price that difference.

Onchain credit experienced a tremendous growth during the last year

The Cracks in the Foundation

The honest account of on-chain credit in 2026 includes the stress signals, not just the growth narrative.

Fitch Ratings reported that the US private credit default rate rose to 5.8% in January 2026, continuing its upward climb. The First Brands collapse — an auto parts maker that filed for Chapter 11 in September 2025 after failed refinancing and the discovery of complex, undisclosed off-balance sheet liabilities — hit a range of private lenders hard, with many lacking clear visibility into leverage and collateral quality until it was too late.

On-chain infrastructure doesn't eliminate that credit risk entirely. Tokenized private credit pools have baseline default rates in the same broad 1% to 3% annualised range as TradFi mid-market direct lending. What it changes is transparency and speed of price discovery — a poorly underwritten loan pool shows up in secondary token pricing before it shows up in a quarterly NAV report.

That's valuable, but it's not the same as risk reduction. Maple Finance CEO Sidney Powell expects on-chain credit defaults to test the system in the coming years, arguing that transparent, auditable blockchains will ultimately make private credit markets safer — but the stress test hasn't arrived at scale yet.

The regulatory picture is also still forming. The SEC's January 2026 joint staff statement on tokenized securities confirmed that tokenization does not change the legal nature of the underlying asset: therefore, a tokenized fund interest is still a security, subject to the same framework as its traditional equivalent. That clarity is useful for permissioned institutional products. However, for permissionless DeFi integration of private credit tokens — the direction the market is moving — the regulatory question is still open.

The Scale of What's Coming

The global private credit market stood at $3 trillion at the start of 2025, up from $2 trillion in 2020, and is estimated to reach $5 trillion by 2029. Keyrock estimates the gradual growth of on-chain private credit to $15–17.5 billion by the end of 2026. Even at the upper end of that forecast, on-chain credit represents less than 0.5% of the total private credit market. The penetration rate tells you that the growth story is still in its earliest chapters.

The defining theme of 2025 was that tokenization finally became a distribution technology that institutions were willing to use at scale. Looking ahead, continued institutional participation is likely to deepen as the product spectrum widens. Further integration with lending markets and on-chain treasury systems will increase both the usefulness and appeal of RWAs, positioning tokenization as a central pillar of digital capital markets.

The $300 billion in stablecoins seeking real yield represents a permanent structural shift rather than a cyclical phenomenon — the market has decisively outgrown its available instruments. On-chain credit offers the most compelling resolution DeFi has produced: exogenous yields untethered from crypto volatility, continuous liquidity mechanisms operating across all time zones, and transparent loan performance visible in real-time. The market has rendered its verdict through capital allocation — growth from $252 million to over $5 billion represents validation at scale, not speculation at the margins.

The question has evolved beyond product-market fit. What remains uncertain is whether underwriting infrastructure, regulatory frameworks, and secondary market depth can mature at the pace capital demands — and whether all three can withstand the stress of the default cycle that inevitably follows this rate of expansion.

To learn more about onchain private credit:

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.