Revealing the Types of Players in the Tokenization Industry

Most coverage of the tokenization market treats it as a single thing – a homogenous wave of blockchain adoption washing over traditional finance. That framing misses the structure entirely: tokenization is not a single market. Here's the actual structure.

The Layers of the RWA Industry

The industry's credibility problem – and its largest near-term opportunity – both live in that confusion. The players who understand which layer they're building for will capture the next decade of growth. Those who conflate them will face correction when the market develops the analytical sophistication to price the difference.

It's three distinct markets, serving three different types of participants, with different products, regulatory requirements, risk profiles, and definitions of what "ownership" actually means.

Institutional investors held 69.1% of the asset tokenization market in 2025, while the retail segment is advancing at 50.2% by 2031. Those two numbers coexist because they describe different layers of the same industry – and conflating them produces the kind of analysis that sounds comprehensive while explaining very little.

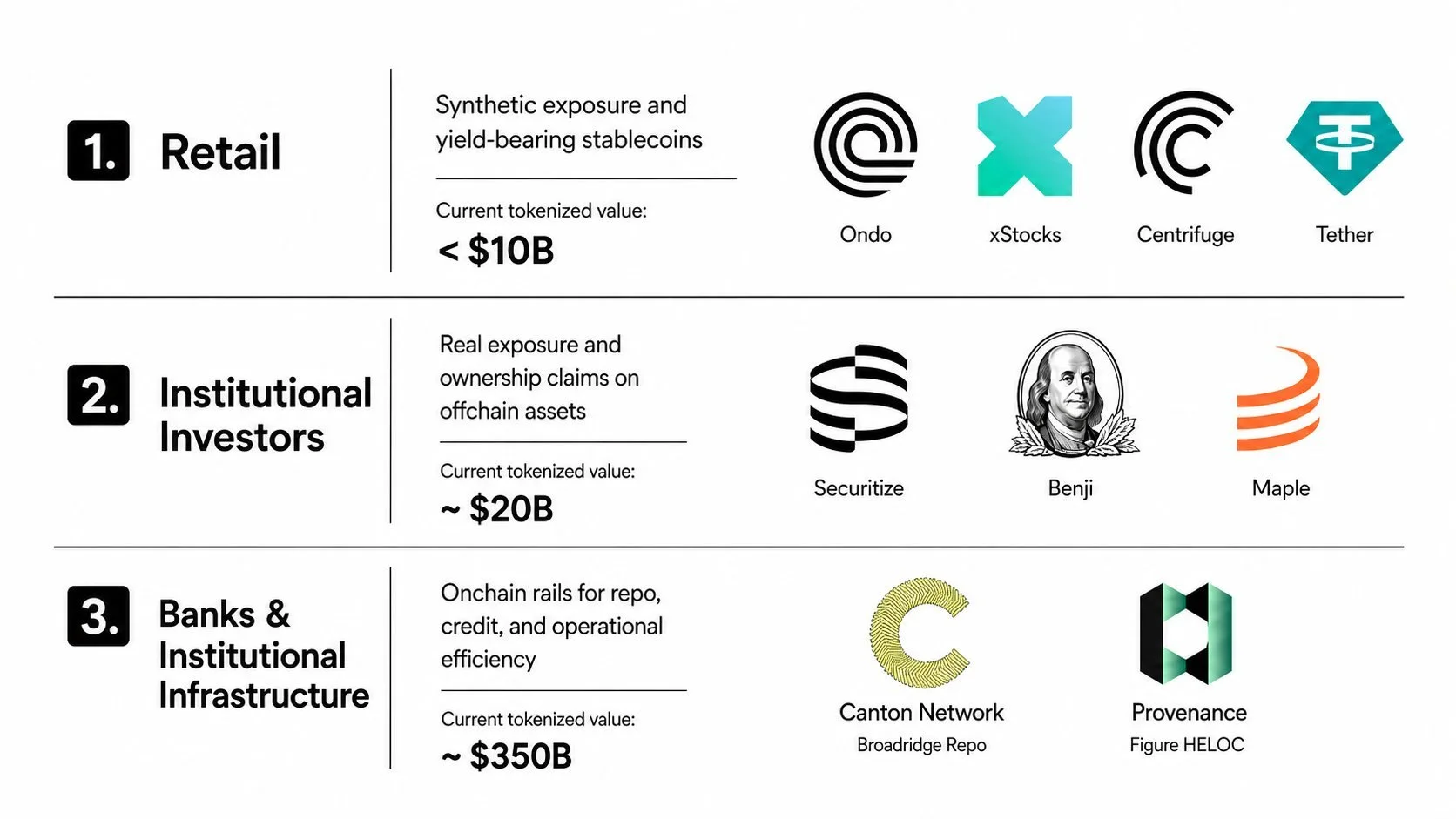

Layer One: Tokenization for Retail

The description is simple: no KYC, accreditation requirement, or custodian account in a foreign jurisdiction. A client just needs a wallet and an Internet connection.

Retail tokenization is not, in most cases, direct ownership of an underlying asset. It's price exposure – synthetic instruments that track the performance of stocks, commodities, or indices without conferring the legal ownership rights that come with holding the actual asset. Ondo Finance's $AAPLon tracks Apple's stock price, while Tether's $XAUT is pegged to physical gold held in vaults, and none of these requires a brokerage account, a KYC process, or a minimum ticket above a few dollars.

Over 60% of retail and institutional investors are already investing in or planning to invest in tokenized assets, with retail platforms like Robinhood and Coinbase offering tokenized private equities, including fractional OpenAI shares – though these often omit voting rights and carry regulatory risk. The omission of voting rights is the structural tell: retail tokenization gives you the economic exposure, not the ownership claim. That distinction is intentional – it's what makes the product globally accessible without triggering securities registration requirements in every jurisdiction.

The yield-bearing stablecoin is the retail tokenization product that has scaled fastest and most quietly. Holding USDC in a Coinbase account that earns 4.5% APY is, functionally, a tokenized money market position. The user doesn't think of it that way, but the economics don't care what the user thinks of it.

The retail layer is where the holder count is growing fastest – and where the Stripe moment for tokenization is most visible. The retail segment is advancing at 50.2% CAGR to 2031 – faster than the institutional layer, from a smaller base, with products that require no minimum ticket and no prior financial sophistication.

Layer Two: Tokenization for Institutional Investors

Here’s another level: KYC required, as well as accreditation or professional investor status. Direct ownership claims on real underlying assets.

This is where the products that dominate RWA coverage live. BlackRock's $BUIDL is a tokenized money market fund – a direct ownership interest in a portfolio of US Treasury securities, held on-chain, accruing yield daily, redeemable in near-real-time for USDC. Franklin Templeton's $BENJI has the same structure across Stellar and Polygon. Maple Finance's institutional pools are senior-secured credit facilities with professional investor access, full loan documentation, and on-chain yield distribution.

There are over 200 active institutional RWA token initiatives with participation from more than 40 major financial institutions, with 86% of surveyed institutional investors having exposure to or intending to allocate to digital assets. The institutional layer is where the capital is – 69.1% of the tokenization market share by value sits here, and where the credit rating infrastructure being built by Moody's TIE will have its most immediate impact.

The structural difference from the retail layer is legal rather than technical. A $BUIDL holder has a legal ownership claim on the underlying Treasury portfolio, enforced by Securitize's transfer agent function and governed by SEC-regulated fund documentation. An $AAPLon holder has a synthetic price exposure governed by smart contract mechanics. Both exist on-chain, but the legal architecture is entirely different.

This distinction matters because it determines what happens in a stress scenario. When a tokenized fund faces redemption pressure, the legal documentation governs what happens to the underlying assets. When a synthetic token faces selling pressure, the smart contract mechanics govern what happens to the price peg. These are not equivalent risks – and the market is only beginning to develop the analytical frameworks to price them differently.

High-net-worth individuals and institutional investors plan to allocate 8.6% and 5.6% of their portfolios, respectively, to tokenized assets by the end of 2026. That allocation, at current global AUM levels, represents an inflow that would multiply the current $30 billion distributed RWA market several times over. The infrastructure being built at Layer Two is the primary beneficiary.

Layer Three: Tokenization for Banks and Institutional Infrastructure

A totally different story: no retail access or individual investor KYC possible. This is the plumbing layer – infrastructure for financial institutions to bring their own operational processes on-chain.

Broadridge's repo market operations on the Canton Network process $60 billion in average daily volume through tokenized repo agreements that settle in near-real time. The end borrower never touches a blockchain, while the capital markets infrastructure behind their loan does.

In 2026, banks are deploying tokenized deposits for institutional and wholesale use cases, designing architectures that coexist with CBDCs and stablecoins. Tokenized deposits are establishing themselves as the settlement backbone for tokenized asset ecosystems. JPMorgan's Kinexys processes $2 billion in daily transaction volume – intraday repos, cross-border payments, tokenized collateral transfers – entirely between institutional counterparties. No retail investor participates, but the retail banking customer's experience is unchanged. The wholesale infrastructure behind it has been rebuilt on digital rails.

Permissioned blockchains captured 50.6% of the tokenization market in 2025 – and networks are forecast to grow at 51.6% CAGR but from a smaller base. The permissioned dominance reflects Layer Three's requirements: institutional infrastructure needs privacy, controlled access, and regulatory certainty that public blockchains don't currently provide for all use cases. Canton Network, Broadridge's LedgerEdge, and JPMorgan's Kinexys all operate on permissioned or private architectures for exactly this reason.

The Layer Three opportunity is also the largest by addressable market. Global repo markets alone process $10+ trillion daily. Global bond settlement runs through DTCC at $4.7 quadrillion annually. Moving even a fraction of those flows to tokenized rails – which is what the DTCC's July 2026 production launch is designed to begin – represents a market opportunity that makes the current $30 billion distributed RWA figure look like a rounding error.

Why the Distinction Matters

The three-layer framework is not academic, as it has direct implications for how to evaluate products, assess risk, and understand where the market is actually going.

Asia-Pacific is set to record tokenization during 2026–2031 – the fastest-growing region globally – across all three layers simultaneously. Retail synthetic tokens are gaining adoption in markets where traditional brokerage access is limited. Institutional tokenized credit is attracting family office and wealth management capital through Singapore and Hong Kong. Bank infrastructure tokenization is advancing through Project Guardian and the HKMA's Project Ensemble. Metafyed operates at Layer Two – and that choice is deliberate.

Layer One offers price exposure without legal ownership. Layer Three operates between institutional counterparties at ticket sizes that exclude most of the market. Layer Two is where genuine ownership meets genuine accessibility: a Singapore investor holding a direct legal claim on a Manila receivables pool yielding 12% in USD, from a $100 minimum ticket, with full KYC and on-chain yield distribution.

That's the gap we built for. Not synthetic exposure, not wholesale bank infrastructure – direct ownership of institutional-quality private credit in Southeast Asia, at a minimum ticket that didn't exist three years ago.

The players who understand which layer they're building for – and design their products, compliance infrastructure, and distribution accordingly – are the ones who will capture the growth. The players who treat tokenization as a single market, or who build a Layer One product and market it with Layer Two credibility claims, are the ones who will face the correction when the market develops the analytical sophistication to price the difference.

Tokenization will eventually eat TradFi. The three layers describe how – from the bottom up, from the top down, and from the edges in, simultaneously.

Explore how Metafyed is doing tokenization the right way:

Visit our website I Follow us on X I Join the Telegram Community

This article is intended for general informational purposes and should not be construed as financial, investment, or legal advice.